In August 2025, a research team at MIT published a number that should have stopped every boardroom AI project cold. After studying more than 300 enterprise deployments, the MIT NANDA initiative found that 95% of enterprise generative-AI pilots delivered no measurable return. Not a small return. No measurable return at all.

The finding landed quietly, then spread through finance departments like cold water. Here were companies that had bought the licenses, run the pilots, sat through the demos, and watched their investment produce nothing they could point to on a profit-and-loss statement.

If you run a small or medium business in Europe and you have felt that same quiet disappointment with AI, you are not behind. You are in the majority.

The numbers tell a brutal story. Independent of any vendor, McKinsey found that only around 39% of organizations report any bottom-line impact from AI, and for most of them the impact is under 5%. Boston Consulting Group put it more bluntly: 74% of companies show no tangible value from AI at all. Meanwhile a small group pulls away. An IDC study commissioned by Microsoft found that the leading firms earn a 2.84 times return on their AI investment, against just 0.84 times for the laggards.

This article is about that gap, and about the one thing the winners have that the rest do not. It is not a bigger budget. It is not a better model. It is readiness. And once you understand what readiness actually means, the gap stops looking like a wall and starts looking like an opening.

Because here is the part the hype merchants leave out: the reason most AI projects fail has almost nothing to do with the AI.

The gap is real, and it is widening

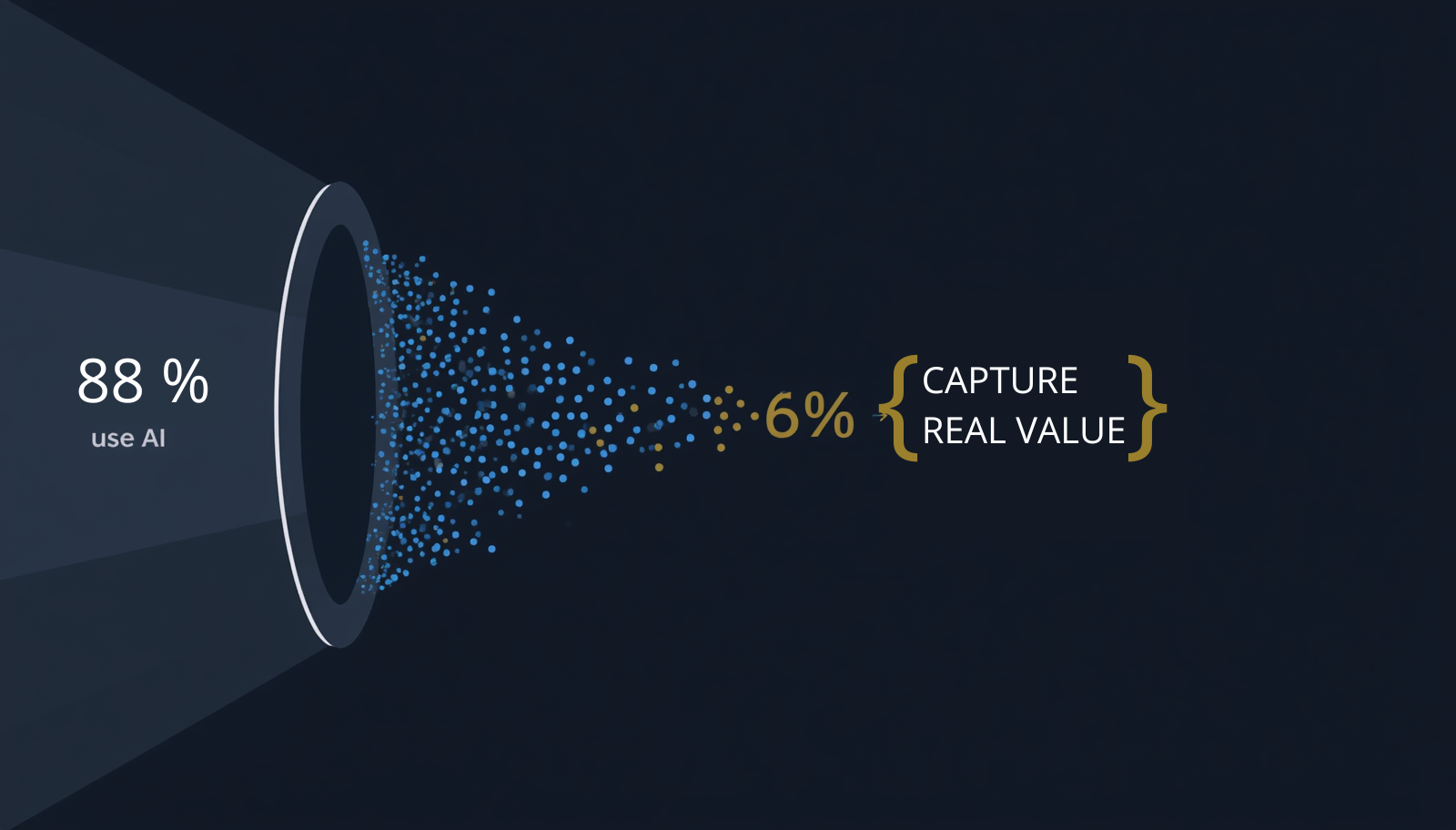

Start with adoption, because the story usually gets told backwards. AI is not rare. Across the EU, around 20% of enterprises used AI in 2025, up from 13.5% the year before. Denmark leads the entire union at 42%, nearly double its 2024 figure. Look at large companies alone and the numbers climb higher still. Globally, 88% of organizations now use AI in at least one function.

So access is not the problem. Almost everyone has touched AI. The problem shows up at the next step, when access is supposed to turn into value.

That is where the crowd thins out fast. Gartner predicted that at least 30% of generative-AI projects would be abandoned after the proof-of-concept stage by the end of 2025. McKinsey counts only about 6% of firms as genuine "AI high performers". BCG counts just 26% that have moved past pilots to real, scaled value.

Put those figures next to each other and a shape appears. A large majority experiments. A thin minority profits. The distance between them grows every year, because the firms that figure it out compound their advantage while everyone else restarts the same failed pilot with a newer model.

For European SMBs the shape is sharper still. The gap between large and small firms is enormous: 55% of big EU companies use AI, against 17% of small ones. The union has set itself a target of 75% of enterprises using AI, cloud, or big data by 2030, and on current trends AI is the piece dragging behind. That target will be won or lost in the small and medium businesses that make up most of the European economy.

Buying tools is not the same as being ready

Here is the trap almost every company walks into. AI arrives as a product. A licence. A per-seat price. A logo in the corner of software you already use. So it gets treated like any other software purchase: approve the budget, buy the seats, send an email announcing the rollout, and wait for the productivity to appear.

It does not appear. The licences sit mostly unused, the pilot quietly winds down, and a year later someone in finance asks what the return was.

The MIT researchers who found that 95% failure rate were clear about the cause. The pilots did not fail because the models were weak. They failed because of how companies tried to use them. Value showed up when firms rebuilt a specific workflow around the tool, and stayed absent when they simply bolted the tool onto how they already worked.

BCG reached the same conclusion from a different angle and turned it into a rule of thumb. In the companies that actually get value from AI, only about 10% of the effort goes into algorithms and models, 20% into technology and data, and a full 70% into people and process. The maths is uncomfortable for anyone hoping to buy their way to readiness. The part you can purchase is the small part. The part that decides whether it works is the part no vendor can sell you.

Gartner's data points the same direction. The organizations most satisfied with their AI results were the ones that spent roughly 30% more on data, governance, and talent, not on models. And 63% of organizations either lack the right data management practices for AI or are not sure whether they have them. A brilliant model pointed at disorganized data produces confident nonsense, faster.

None of this is a reason to avoid AI. It is a reason to stop treating a Copilot licence as a strategy. The tool is real and useful. It is just the last 10%, not the first step.

What the few actually do differently

So what separates the firms that get the 2.84 times return from the ones that get nothing? Strip away the vendor language and it comes down to two things working together, not one.

The first is technical. The winners have their data in order, their systems connected, and somewhere sensible for the work to happen. Not perfect, but organized enough that an AI tool can reach clean information and act on it.

The second is organizational, and this is the one almost everyone underweights. The winners changed how work gets done. They picked a real process, redesigned it around the new capability, retrained the people involved, and measured whether it actually helped. McKinsey found that the high performers were far more likely to fundamentally redesign workflows rather than sprinkle AI on top of the old ones.

Readiness is those two axes together. Strong technology and a stalled organization gets you an expensive pilot that nobody adopts. A motivated organization on top of chaotic data gets you enthusiasm that hits a wall. You need both, and most companies are unbalanced on one side or the other. That balance is important enough that it deserves its own article, which is where this series goes next.

The encouraging part, especially if you are small, is what this list does not include. It does not require a hyperscaler budget. It does not require a data-science team. The single most cited barrier to AI across Europe is not cost or technology. It is a lack of relevant expertise, named by 71% of enterprises. That is a skills-and-organization gap. Which means it is a gap an SMB can close with focus, without outspending anyone.

What this means if you are an SMB on a real budget

If you are a European small or medium business, the readiness gap is not bad news. It is the most level playing field AI will ever offer you, for three reasons.

First, the winning ingredients are mostly organizational, and small companies are better at organizational change than large ones. You do not need to align twelve departments and a global IT function. You need to fix one workflow and get a handful of people to work differently. That is a Tuesday for a well-run SMB and a two-year programme for an enterprise.

Second, you can start where the value is highest and the risk is lowest. The firms getting results did not begin with a moonshot. They took one repetitive, document-heavy, rules-based process, the kind every business has, and rebuilt it. Pick the task your team complains about most. Start there.

Third, doing it properly in Europe means doing it in a way that respects the rules from day one, and that is easier when you are small and starting fresh than when you are large and retrofitting. The EU AI Act already requires every organization that uses AI to ensure its staff have a basic level of AI literacy, a duty that has been in force since February 2025. Your data-protection obligations under GDPR do not pause because a tool is clever. Building with governance in mind from the start is not a tax on readiness. As this series will show, it is part of what makes the readiness real. That is the subject of a later article, on why trust is the accelerator rather than the brake.

The honest summary is this. AI will not transform your business because you bought it. It will transform your business if you change how your business works, in one place, on purpose, and then in another. The tool is the easy part. The readiness is the work. And the work is squarely within reach of a company your size.

The MIT number that opened this article, the 95% of pilots that returned nothing, was not a verdict on artificial intelligence. It was a verdict on how companies approached it. The 5% that worked were not using secret models. They were using the same tools as everyone else, wrapped around a business that had made itself ready to use them.

That is the whole game. Not the model. Not the licence. The readiness underneath. Most European companies still have it backwards, spending on the tool and skipping the work, then wondering why the return never comes.

The good news is that the recipe is not a mystery, and it is not reserved for the giants. It is two axes, balanced, applied to one process at a time. In the next article we take the first of those axes apart, and explain why readiness is something you build, not something you buy.